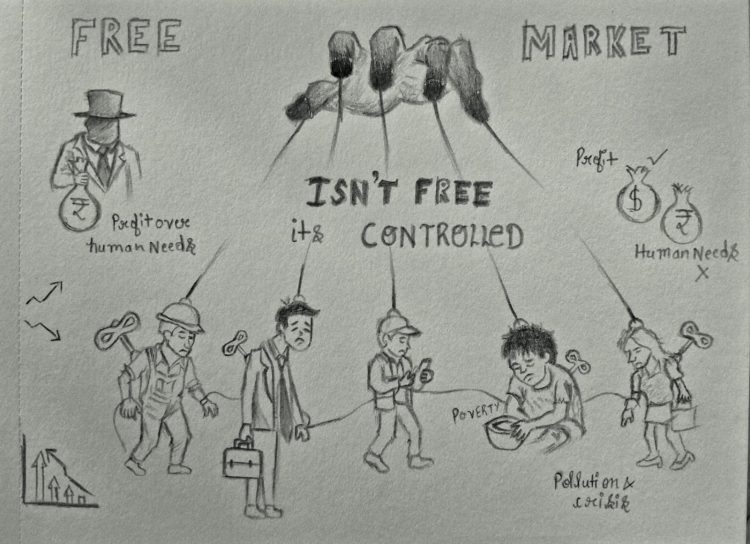

The idea that the free market is a natural, efficient, and self-regulating system is not a conclusion derived from history. It is an ideological claim sustained in spite of history. When examined across centuries and geographies, the empirical record does not show markets emerging from freedom, producing stability, or distributing prosperity. It shows the opposite. Markets are constructed through coercion, stabilized through state intervention, and repeatedly destabilized by their own internal contradictions. What is called the free market is therefore not an economic reality but a theoretical abstraction that conceals the material processes through which power and wealth are organized. To describe it as a travesty of economics is not rhetorical excess. It is an accurate description of a framework that systematically misrepresents the world it claims to explain.

The foundational claim of free market theory, associated with Adam Smith, is that individuals pursuing self-interest within competitive markets generate socially optimal outcomes. This claim rests on three assumptions: that exchange is voluntary, that actors are relatively equal in power, and that markets tend toward equilibrium. None of these assumptions survive historical scrutiny. The emergence of capitalist markets in Europe required the violent separation of producers from their means of subsistence. The enclosure movement in England, spanning roughly the sixteenth to eighteenth centuries, converted common land into private property through parliamentary acts and force. Hundreds of thousands were dispossessed. The result was not a free population choosing to enter markets, but a population compelled to do so. The labour market, the core of capitalism, was born not out of freedom but out of dispossession.

This establishes the first contradiction of the free market: it claims to be based on voluntary exchange, but its very existence depends on coercion. As Karl Marx demonstrated, a labour market requires a class of people who have no option but to sell their labour power. This condition is historically produced, not naturally given. The market does not eliminate power relations. It reorganizes them in a way that appears neutral while preserving structural inequality.

The expansion of markets beyond Europe through colonialism intensifies this contradiction. Colonial economies were not integrated into global markets through mutual exchange; they were forcibly restructured to serve imperial interests. In India, colonial policies dismantled indigenous industries and reoriented agriculture toward export crops. Between 1876 and 1878, a famine killed between 5 and 10 million people. During this period, grain exports continued because global prices made export profitable. The market did not fail on its own terms. It functioned precisely as designed. Food went to those who could pay, not to those who needed it. This reveals the second contradiction: the market claims to allocate resources efficiently, but its definition of efficiency is indifferent to human survival. Profitability, not need, determines distribution.

The industrial revolution is often invoked as evidence of market success. Yet its historical reality undermines this claim. Industrialization depended on cheap raw materials extracted from colonies, technological developments supported by public institutions, and a labour force disciplined through harsh legal frameworks. In early nineteenth-century Britain, factory workers commonly worked 12 to 16 hours a day under dangerous conditions. Child labour was widespread, and wages hovered at subsistence levels. These were not temporary distortions. They were structural outcomes of competitive accumulation. It was only through prolonged political struggle, including unionization and legislative intervention, that basic protections were established. Regulation did not create inefficiency; it prevented social collapse.

The tendency of markets toward concentration further contradicts their theoretical premises. Free market theory assumes sustained competition. Historical development shows the opposite. By the late nineteenth century, economies in the United States and Europe were dominated by monopolies and trusts. In the contemporary period, a handful of corporations control vast segments of global production and exchange. This is not an aberration; it is a logical outcome of competitive accumulation, where larger firms absorb or eliminate smaller ones. The market does not disperse power; it centralizes it.

The twentieth century provides decisive evidence of systemic instability. The Great Depression saw global industrial output fall by approximately 38 percent between 1929 and 1933, while unemployment in the United States reached nearly 25 percent. Markets did not self-correct. Prices fell, production contracted, and demand collapsed in a downward spiral. Classical economic theory, built on equilibrium assumptions, offered no explanation or solution. Recovery required large-scale state intervention, guided by the ideas of John Maynard Keynes. Public spending, financial regulation, and welfare programs stabilized economies that markets had destabilized. This establishes the third contradiction: markets claim to be self-regulating, but in moments of crisis they depend on external intervention to survive.

The reassertion of free market ideology in the late twentieth century under neoliberalism did not resolve these contradictions; it intensified them. Policies associated with Milton Friedman promoted deregulation, privatization, and the reduction of state involvement in economic life. In practice, these policies increased inequality, weakened labour protections, and exposed economies to volatile capital flows. Structural adjustment programs imposed across Latin America, Africa, and parts of Asia reduced public expenditure on health, education, and welfare while opening domestic markets to global competition. The result was not efficient equilibrium, but social fragmentation and economic vulnerability.

The global financial crisis of 2008 exposed the internal logic of this system with clarity. Financial institutions created complex derivatives tied to subprime mortgages, amplifying risk across the global economy. When the system collapsed, it was not the market that corrected itself. Governments intervened with bailouts totaling trillions of dollars. In the United States alone, the Troubled Asset Relief Program authorized 700 billion dollars, while the Federal Reserve extended far larger liquidity support. Losses were socialized, while gains remained private. This reveals the fourth contradiction: the market claims autonomy from the state, but relies on the state to absorb its failures.

The argument that excessive regulation produces corruption and inefficiency misidentifies the source of these phenomena. Corruption is not generated by the presence of regulation, but by the concentration of economic power. In deregulated environments, powerful actors shape rules, evade accountability, and extract rents. The Gilded Age in the United States, characterized by minimal regulation, was marked by widespread corporate corruption and political capture. The absence of regulation did not produce transparency; it allowed wealth to translate directly into power. Regulation emerges not as a cause of corruption, but as a response to it.

The claim that distrust of business is culturally produced, rather than historically grounded, also collapses under scrutiny. Societies that have experienced dispossession, exploitation, and crisis develop skepticism toward unregulated economic power because such skepticism is empirically justified. This is not a psychological bias; it is a rational response to historical experience. To argue that suspicion creates corruption reverses causality. Exploitative structures produce distrust, not the other way around.

Comparisons with high-income welfare states further undermine free market claims. Economies such as those in Scandinavia are often cited as examples of successful market systems built on trust. In reality, these economies combine market mechanisms with extensive regulation, high taxation, and strong social welfare systems. Labour rights are robust, public services are universal, and income inequality is significantly lower than in more deregulated economies. Their stability is not the result of market freedom, but of institutional frameworks that constrain market outcomes. The idea that markets, left alone, produce socially beneficial behavior is not supported by these examples. Collective outcomes are structured, not spontaneous.

Environmental history exposes the final contradiction. Markets prioritize short-term profitability, leading to the systematic externalization of ecological costs. The accumulation of greenhouse gases, deforestation, and biodiversity loss are not accidental side effects; they are structural consequences of a system that does not account for long-term sustainability unless compelled to do so. Climate change represents a failure not of policy implementation, but of market logic itself. A system oriented toward continuous growth cannot, on its own, preserve finite ecological systems.

Across these historical moments, a consistent pattern emerges. The free market rests on four interrelated contradictions: it claims freedom but depends on coercion; it claims efficiency but produces deprivation; it claims stability but generates crisis; and it claims autonomy but relies on the state. These are not peripheral flaws. They are structural properties of the system.

To understand why the free market is a travesty of economics, one must examine the methodological foundations of the discipline itself. Economic theory abstracts from history, power, and social relations to construct models of rational actors operating in equilibrium. These models treat prices as neutral signals, ignoring the processes through which purchasing power is distributed. They treat outcomes as efficient, even when they reflect unequal initial conditions. In doing so, they convert historically produced inequalities into apparently natural results. Economics, in this form, does not describe reality; it sanitizes it.

The persistence of free market ideology, despite overwhelming historical evidence to the contrary, is itself a phenomenon that requires explanation. It persists because it serves a function. It provides a framework through which existing distributions of wealth and power can be justified as the outcome of neutral processes. It obscures the role of coercion in the formation of markets, the role of the state in sustaining them, and the role of crisis in shaping their trajectory. It transforms contingent historical arrangements into universal principles.

World history does not show that free markets work. It shows that they cannot work on their own terms. They require continuous intervention to prevent collapse, continuous regulation to mitigate harm, and continuous ideological reinforcement to maintain legitimacy. The question, therefore, is not whether markets should exist, but whether they should be treated as the organizing principle of society. History provides a clear answer. When markets are allowed to dominate social life, they reproduce inequality, generate instability, and undermine the conditions necessary for human survival. That is not a failure of execution. It is the logical outcome of the system itself.